2020 var det första helår där jag gick in i året med ett stort fokus på att själv ta hand om min aktieportfölj istället för att förlita mig på vänner eller krama index, efter att ha tagit tag i saken och blivit mer seriös under andra halvan av 2019. Efter att portföljen under brinnande pandemikrasch var ner drygt 40% som värst, vände allting under andra halvan och året slutade minst sagt i dur, med en avkastning om +56%, långt över alla relevanta jämförelseindex (men långt under många av de sanslösa avkastningar man matats med på Twitter senaste veckan).

Det hade varit väldigt lätt att slå sig för bröstet och intala sig själv att man gjort en fantastisk insats när jag lyckas nå denna fina avkastning under det första helår då jag själv arbetat mer aktivt med portföljen. Jag är dock av den åsikten att detta i mitt (och många andras) fall hade varit ett stort misstag, av flera anledningar. Dels gör jag inte särskilt många affärer på ett år, så att bedöma hur pass bra jag är som investerare på ett enstaka års utfall innebär att man bedömer mig på ett väldigt litet urval av affärer, men en ännu viktigare aspekt är att en väldigt stor del av min avkastning under året kommer från innehav som jag ägt sedan 2017 (Enlabs) respektive 2018 (Gravity), båda case där jag inte alls var delaktig i att göra grundjobbet utan förlitade mig på mina goda vänners kunskap och goda omdöme. Den i min mening absolut viktigaste aspekten, som jag upplever att många helt förbiser, är av mer övergripande och teoretisk natur, nämligen slumpens/turens inverkan på ens utfall över såpass kort tid som ett år faktiskt är.

Sannolikheter > determinism, Process > utfall,

Utfallet av en investering, precis som utfallet av en pokerhand eller en hockeymatch påverkas till stor del av slumpmässiga faktorer som ligger utanför utövarens kontroll. En pandemi kan slå till, ett dåligt riverkort kan komma på brädan, en domare kan döma absurda utvisningar åt ena lagets håll, etc. Vi människor är av evolutionen stöpta för att hela tiden leta efter mönster och dra kausala samband. När vi får ett utfall presenterat för oss skapar vi omedelbart och omedvetet ett kausalt samband. Y skedde därför att jag gjorde X. Vi är deterministiska till naturen.

I aktiviteter som till 100% påverkas av skicklighet är detta korrekt, men i alla aktiviteter där slump/tur har en stor påverkan på utfallet, kommer våra analyser att bli sanslöst dåliga. Vi drabbas väldigt lätt av ”hindsight bias”, alltså att vi, när vi väl vet utfallet, menar på att det var tvunget att bli så och att vi minsann hade kunnat säga det på förhand, eller rentav att vi sa det på förhand (även fast vi oftast inte gjorde det, så duktiga är vi människor på att vilseleda oss själva).

Istället måste vi se investeringar som ett spel om sannolikheter med en obegränsad mängt potentiella utfall. Låt oss ta Gravity som exempel. Bolaget har under 2020 släppt två stora titlar som båda initialt verkar vara succésläpp. Visst kan man på förhand försöka göra skaffa sig så mycket information som möjligt för att kunna göra en bedömning om hur framgångsrika dessa spel kommer att bli, men det är helt omöjligt att med säkerhet veta hur dessa spel kommer att tas emot, om servrar kommer palla trycket osv, på förhand. Utfallet av dessa spelsläpp har hittills blivit precis så bra som man hade kunnat hoppas på, utfallet har varit i den absoluta toppen av potentiella utfall, vilket också lett till att aktiekursen rusat under året. Att slå mig själv på bröstet och deklarera vilken fantastisk investerare jag är baserat på detta vore helt fel. Detta utfall är bara ett av ett obegränsat antal potentiella utfall som hade kunnat ske, så att bedöma min insats baserat på just detta utfall är en analysmetod som med säkerhet kommer leda till felaktiga slutsatser.

Som ett annat exempel kan vi ta Points International, ett bolag som säljer VIP-programspoäng, främst åt flygbolag och hotell, som jag ägde tidigt under 2020, och som jag sålde med förlust tidigt under pandemin. Var det ett dåligt beslut att investera i detta bolag? Kanske, kanske inte, men det är åtminstone enkelt att se att detta utfall, en global pandemi som lamslår hela resebranschen, är ett extremt utfall som inte hör till de vanligaste. Att kritisera min investering i bolaget baserat på just detta utfall är givetvis lika fel som att ta hela äran för min lyckade investering i Gravity. Det är otroligt viktigt att inse att man kan göra en dålig investering, men få ett fantastiskt utfall, precis som man kan göra en bra investering, men få ett riktigt uselt utfall. Gör man investering där man i 90% av fallen kommer att tjäna 100%, men i 10% av fallen förlora 100%, och utfallet råkar hamna i de negativa 10%, har man ändå gjort en otroligt bra investering som man kommer att tjäna mycket pengar på i längden. Vi måste tänka i sannolikheter, och inte i efterkonstruerade kausala samband.

Det är förhoppningsvis tydligt att vi därför inte kan utvärdera vår prestation som investerare baserat på utfallet i specifika affärer, och gör man inte särskilt många affärer tar det lång tid innan man får ihop ett tillräckligt stort urval för att med statistisk säkerhet kunna säga någonting om en investerares skicklighet. Hade man stoppat 100% av portföljen i EVO eller Tesla vid årets start hade man haft en sagolikt börsår med tresiffrig avkastning. Men är man en bra investerare?

Så om vi inte kan utvärdera vår insats baserat på utfall, hur kan vi då utvärdera vår insats överhuvudtaget? Svaret, enligt mig, är att fokusera intensivt på att utvärdera processen som ledde fram till investeringen. Vilken information hade jag tillgänglig när jag gjorde investeringen? I ljuset av denna information, tänkte jag på ett rimligt sätt och hade jag sannolikheterna på min sida? Gav jag någorlunda korrekta sannolikheter till de olika utfallen? Det är även här otroligt lätt att i efterhand påverkas av utfallet i sin analys och ge för stor sannolikhet till det utfall som faktiskt inträffade, och för små sannolikheter till de utfall som inte inträffade. Ett hjälpmedel mot detta kan vara att förlita sig på base rates, d.v.s. att utgå ifrån hur vanliga de olika utfallen faktiskt är om man tittar på en större population snarare än just det bolaget vi undersöker. Forskningen inom beteendeekonomin visar att vi människor lägger alldeles för stor vikt vid den specifika detaljerade informationen om just vårt fall, och för lite vikt vid de genomsnittliga sannolikheter som gäller för att något ska inträffa. Ett annat hjälpmedel kan vara att föra en noggrann dagbok över sina investeringsbeslut, både de bolag man undersöker och faktiskt investerar i, samt de bolag man undersöker och väljer att inte investera i. Jag försöker att för varje bolag jag tittar på avsluta med en kort sammanfattning om varför jag väljer att investera eller inte, och en ungefärlig riktkurs på vad jag tycker bolaget bör vara värt. Detta kan jag sedan gå tillbaka till och titta på i efterhand för att se hur processen såg ut just vid analystillfället. För varje uppdatering av riktkursen gör jag en ny sammanfattning som följer den tidigare så att jag kan följa min tankeprocess och hur mina antaganden förändras längs vägen.

”I know” vs ”I don´t know”

I ett avsnitt av Value After Hours (orkar inte leta upp vilket) som jag lyssnat på under året gjorde Jake Taylor en intressant distinktion mellan två typer av investerare, ”I know”-investerare och ”I don´t know”-investerare.

Investarere av typen ”I know” har stor tilltro till sin förmåga att se framtiden utspela sig och att hitta den stora framtida vinnaren, oavsett om det är makroekonomiska faktorer eller hur specifika branscher kommer att utvecklas. Dessa investerare tenderar att föredra tillväxtbolag där en stor del av vinsterna ligger långt fram i tiden, eftersom man litar på sin förmåga att pricka rätt vinnare.

Investerare av typen ”I don´t know” är mer skeptiska till sin egen (och i många fall även andras) förmåga att förutspå saker särskilt långt fram i tiden. Den här typen av investerare bettar mer sannolikt på ”status quo” i högre utsträckning, eller att saker ska förändras mindre än vad som allmänt förväntas i vissa branscher, och föredrar lägre värderingar där en större del av kassaflödena ligger i närtid och starka balansräkningar som utgör krockkudde.

Personligen tillhör jag definitivt kategorin ”I don´t know”. Detta är säkerligen delvis ett personlighetsdrag, delvis en effekt av att jag läst värdeinvesteringsböcker från och till i tio års tid, men framför allt en effekt av mitt yrke och mitt stora intresse för beteendeekonomi och prognoser. Som statistiker/dataanalytiker vet jag hur svårt det är att prognosticera med särskilt hög träffsäkerhet, och detta syns även tydligt i empiriska studier. Philip Tetlock, författaren bakom den fantastiska boken ”Superforecasting” har vigt sitt liv åt att studera prognoser, och hans slutsats är att alla prognoser som sträcker sig längre fram i tiden än fem år är helt utan värde. Fem år framåt i tiden eller mindre kan vi göra någorlunda ok förutsägelser men därefter är vi hopplöst usla. Det hjälper heller tyvärr inte om vi är experter på området, då experter tvärtom ofta är sämre på att prognosticera då de har för stor tilltro till sin egen förmåga och litar för mycket på den, istället för att, som tidigare nämnt, förlita sig mer på genomsnittliga sannolikheter för en större population.

Av dessa anledningar faller det sig naturligt för mig att leta efter investeringar med låga värderingar som kan räknas hem på kortare tid, eller branscher som är mer osannolika att förändras, där historiken är lång eller speciella branscher som av någon anledning har inslag av monopol eller oligopol. Om vi knyter an till sannolikhetstänket ovan föredrar jag självklart även investeringar där en större andel av de potentiella utfallen ger en acceptabel avkastning, vilket jag ser som en säkerhetsmarginal. Det finns antagligen bolag där ute som värderas till 20x Sales eller mer som kan komma att bli bra investeringar på sikt, men dessa kommer jag att missa, av just den anledningen att det krävs att dessa bolag träffar något av de sällsynta, riktigt bra utfallen för att så ska bli fallet, och så säker på min sak kommer jag i ljuset av den empiri som finns aldrig att vara på min egen förmåga att hitta just det bolag där inget kommer gå fel, för det har man inte råd med till dessa värderingar. En fråga många bör ställa sig som haft fantastiska resor i enskilda aktier som gjort 300% på ett eller ett par år, är vad som hade krävts för att få ett väldigt annorlunda utfall, och hur sannolikt det faktiskt var att något av dessa sämre utfall hade kunnat utspela sig?

Summering av året

Så hur summerar jag då mitt år? Självklart genom att titta på processen.

Det finns saker jag är nöjd med, som att jag aldrig övervägde att sälja av under raset med nån form av tanke att ”tima marknaden”. Även här är de empiriska studierna väldigt eniga i att det är helt omöjligt, så tror man att man är kapabel till detta lurar man antagligen sig själv å det grövsta. Jag är också nöjd med att jag hållit disciplinen och inte släppt på mina principer om värderingar, även om det stundtals varit lockande. Tack vare raset lyckades jag fiska upp ett bolag som jag länge haft på radarn men vars kurs jag inte tyckte gav tillräcklig säkerhetsmarginal innan kursen slaktades under pandemin, där är jag nöjd att jag inte fuskade och köpte trots en värdering som i mina ögon bara var lite för hög.

Det finns också saker jag är missnöjd med. En sådan är att jag under nämnda ras spenderade för mycket tid med att paniskt uppdatera flöden för att få senaste nyheterna, som inte gav någonting i investeringssyfte, istället för att lägga ner precis all tillgänglig tid på att försöka förstå och värdera några potentiellt högkvalitativa bolag som slaktades kursmässigt under raset. Det var tid som inte var väl spenderad och där jag garanterat hade högre timlön på annat håll.

Jag är även missnöjd med att jag vid ett tillfälle under raset brast i min disciplin kring att verkligen tycka att jag förstår de bolag jag äger. Jag köpte ett bolag som jag misstänkte var ett fint bolag vars kurs slaktats, men utan tillräcklig förståelse för hur branschen faktiskt fungerar. Detta insåg jag snabbt och sålde av innehavet bara efter några dagar utan att något förändrats i grunden för bolaget, till en förlust. Oavsett om jag hade gjort en vinst eller förlust i innehavet var processen dålig, eftersom jag anser mig ha för dålig kunskap om den branschen för att äga något bolag i den för tillfället. Jag är också rädd att jag, om kursen hade gått upp istället för ner under tiden jag ägde bolaget, inte hade sålt utan kanske rentav hade klappat mig själv på axeln för en bra affär. Hjärnan gör vad hjärnan gör 🙂

Slutligen vill jag poängtera att jag inte vet huruvida jag är en bra investerare eller inte. När jag väl skriver om bolag på den här bloggen är det inte för att ge råd, utan för att få input på mina tankar och resonemang för att ifrågasätta dessa och se om jag missat något i caset. Jag vet dock en del om att fatta beslut, och att utvärdera beslut som fattas med inkomplett information och där turen spelar en stor roll för utfallet. Detta är lärdomar som kan appliceras både på investeringar men även i ett gäng andra sammanhang, så förhoppningsvis känner ni läsare er ok med att ta till er de principerna, oavsett min förmåga som investerare.

Disclaimer: Informationen i denna text är inte att anse som någon form av investeringsråd utan är mina egna tankar och funderingar kring bolaget. Jag är inte en professionell investerare. Gör alltid din egen analys innan du köper eller säljer aktier. Jag äger för närvarande aktier i Catella och kan köpa/sälja aktier i bolaget utan att meddela bloggens läsare.

I fredags rapporterade Catella, ett av mina klart stökigare innehav. Varje gång jag sitter med bolaget är det samma visa, det känns krångligt, svårt och spretigt och min förståelse för verksamheterna är inte djup. Sen kommer man till värderingen och inser att det ser väldigt billigt ut.

Tf VD och storägare Johan Claesson skrädde inte orden under dagens conf. call utan var djupt kritisk mot prestationen inom flera av bolagets områden och hur avvecklingen av bankverksamheten skötts. Bolaget har ett riktigt svagt H1 bakom sig där Corporate Finance påverkats negativt av corona och Equity, Hedge and Fixed Income funds presterat osedvanligt uselt på fondsidan.

Trots motvinden har man dock gjort 111M i EBIT i de kvarvarande verksamheterna under H1 (dock inkl Mutual Funds som man kommer sälja 70% av under Q3), detta tack vare Property Investment Management som presterar mycket starkt för tillfället. Börsvärdet efter dagens tapp är 1.74 miljarder, man har en liten nettoskuld så låt säga 1.75md

EV. 2017-2019 var EBIT i kvarvarande verksamheterna 481, 440, 454 miljoner så va 460M i snitt, vilket ger EV/EBIT under 4. Det är sannolikt för aggressivt att förvänta sig EBIT på dessa nivåer framgent då man haft stora utflöden ur fonderna i Equity, Hedge & Fixed Income funds efter den svaga prestationen senaste året, samt sålt 70% av Mutual funds (som ingår i detta segment). Under H2 kommer man bokföra försäljningen av Grand Central vilket kommer ge en positiv effekt i bokföringen om 155M.

Verksamheterna är svårprognosticerade för mig, men Corporate Finance brukar alltid ha Q4 som överlägset starkaste kvartal, och man förväntar sig att en ännu större andel av affärerna än vanligt kommer att ske i Q4 i år jämfört med tidigare, och underförstått att Q3 kommer bli svagare än vanligt. YTD har man förlorat 16M på EBIT-nivå i denna del, 2019 gjorde man totalt 62M i EBIT varav 3M första halvåret. Förhoppningsvis är det inte aggressivt att tro att man kommer att göra ~10M EBIT för helåret.

PIM har haft ett mycket starkt H1 med EBIT på 117M att jämföra med 104M för helåret 2019. Däremot har denna del haft Q2 som överlägset starkaste kvartal de senaste åren, ifjol kom över 60% av EBIT under H1. Om vi säger att PIM gör 60M EBIT under H2 är det förhoppningsvis konservativt.

Equity, Hedge & Fixed Income funds har gjort 26M EBIT under H1 vs 181M under H1 2019. Fonderna har gått uselt med stora utflöden, och nu har man även sålt 70% av Mutual funds. Jag har ingen aning hur mycket pengar man kommer tjäna i denna del under H2, men sätter man den till 0 får man ändå en EBIT i H2 på 155M från försäljningen av Grand Central, 10M från Corpen och 60M från PIM (de två sistnämnda förhoppningsvis lågt räknat) = 225M. Adderar vi de 111M från H1 får vi 336M -> EV/EBIT drygt 5.

Blickar vi dessutom fram emot 2021 kommer avvecklingen av banken att slutföras, vilket kommer frigöra likvida medel om 350-400M. Under H2 2020 slutförs även försäljningen av Grand Central och försäljningen av Mutual funds, vilket tillsammans torde inbringa åtminstone 200M. Räknar vi slarvigt bort dessa likvider från dagens EV är vi nere i på runt 1.2 miljarder, att jämföra med historisk EBIT kring 460M och en EBIT för 2020 på 330M-ish. Vad EBIT kommer ligga på i framtiden är imo svårt att vara särskilt exakt kring, men även om framtida EBIT droppar till 250M betalar man ändå under 5x EBIT.

Det finns dock försvårande omständigheter kring att använda EV/EBIT som värderingsmetod. Kassan idag är över en miljard, men enligt Claesson ligger en stor del av dessa pengar i dotterbolag som behöver dessa av regleringsskäl, så dessa står inte moderbolaget fritt att förfoga för att exempelvis dela ut till ägarna. Han flaggar dock för att man kommer ha mer spelrum efter att pengarna från bankförsäljningen kommer in då dessa bör stå moderbolaget fritt att använda till vad man vill.

Dessutom har bolaget en ineffektiv skattestruktur där man av någon anledning som står över min kunskapsnivå verkar ha svårt att kvitta vinster och förluster i olika dotterbolag mot varandra på moderbolagsnivå. Konverteringen av EBIT -> nettovinst och i förlängningen andel av vinst som tillfaller moderbolagets ägare är därför lägre än normalt.

Vi kan även lägga till de faktum att det varit rejäl omsättning på ledningssidan senaste året. Inom loppet av ett par månader under slutet av 2019 sade både fd VD Knut Pedersen och fd CFO Marcus Holmstrand upp sig. Tf CFO Eva Bång satt på posten i dryga månaden innan hon sade upp sig. Nu har man äntligen knutit till sig en ny CFO, Christoffer Abramson, som kommer med ett starkt CV och en tydlig inriktning mot fastigheter. Någon ny VD har ännu inte presenterats, kanske vill Claesson själv styra skeppet tills han tycker att det åter befinner sig i rätt riktning?

Som sagt, det finns en hel del svårigheter med att analysera detta innehav, men när röken lägger sig under 2021 och bolagets verksamhet och inriktning mot fastigheter blir allt tydligare kommer vi ha ett kapitallätt bolag som handlas till mid single digit EV/EBIT, och då har jag inte ens nämnt de investeringar man gjort i fastighetsprojekt som förhoppningsvis är upptagna på BR till klart mindre än de kommer säljas för. För mig är det väldigt svårt att göra exakta prognoser på framtida intjäning vilket talar emot ett ägande, men för att få Catella att se dyrt ut får man göra extremt negativa antaganden om framtiden, alternativt att man tror att de försiggår något fuffens bakom kulisserna som har lett till den stora omsättningen på ledningspersoner. Caset har försämrats sedan jag först köpte i november 2019 på grund av den mycket svaga prestationen inom Equity, Hedge & Fixed income funds samt coronapandemin som gjort framtidsutsikterna mer osäkra i Corporate Finance-delen, men detta reflekteras även i kursen så enligt mina väldigt preliminära beräkningar anser jag att förväntad avkastning är ungefär samma nu som då, men kanske med något större variation i potentiellt utfall. Detta är dock min högst amatörmässiga bedömning och inget du som läsare bör lägga särskilt stor vikt vid alls.

Som sagt, ett innehav som kanske egentligen är lite för komplicerat för mig, men jag misstänker att det är just därför som möjligheten också uppstått. Intresset för bolaget är lågt med få analytiker som ställer frågor vid varje rapport, och kanske lite för struligt för många att analysera i en tid då alla letar compounders. P.g.a. komplexiteten finns det stor risk att jag både räknat eller tänkt fel i texten ovan, så uppmärksamma mig gärna om du märker några sådana. Jag tar tacksamt emot input på allt ovanstående, och om inlägget väckt ditt intresse för bolaget är det av yttersta vikt att du gör din egen research och inte förlitar dig på min då den riskerar att innehålla alla möjliga typer av felaktigheter i antaganden.

I ett avsnitt av podcasten Focused Compounding nämnde Geoff Gannon nyligen att investeringar i net nets troligen är den strategi som har starkast empiriskt stöd för att generera överavkastning jämfört med index av alla mekaniska strategier. Som statistiker/dataanalytiker triggade detta mitt intresse och fick mig att dyka ner i litteraturen på ämnet och se vad studierna faktiskt säger, och hur de utförts.

Vad är en net net?

Det som idag kallas för net nets definierades först av Benjamin Graham i ursprungsutgåvan av Security Analysis, utgiven år 1934. Den enklaste definitionen är att ta ett bolags omsättningstillgångar, dra bort samtliga skulder och preferensaktier, och sedan dela med antalet utestående aktier för att få NCAV, ”Net Current Asset Value” per aktie. Detta värde jämförs sedan med vad aktien handlas till, och Graham föreslår att köpa bolag vars P/NCAV understiger 0,66. Graham hade dock en något mer komplicerad uträkning för NCAV där han endast tillgodoräknade 75% av kundfordringar och 50% av inventarier i sin uträkning. Ett bolag som handlas till lägre än sitt NCAV per aktie handlas alltså till mindre än vad bolagets omsättningstillgångar är värda, efter att alla bolagets skulder dragits av. Uttryckt på ett annat sätt ger marknaden ett negativt värde till verksamheten i bolaget, och inget värde ges till eventuella materiella tillgångar.

Graham menade att ett bolag inte bör handlas till mindre än vad en ägare i bolaget skulle få i handen om bolaget likviderades idag, och att NCAV utgör ett bra estimat för vad detta belopp skulle vara. Likväl är det rimligt att tro att om bolaget i fråga såldes i en privat affär idag, så skulle priset aldrig understiga värdet på bolagets tillgångar, justerat för skulderna. Ett bolag som handlas till mindre än NCAV bör därför vara så nära vi kan vara på att vara säkra på att ett bolag är undervärderat idag.

Bolag som värderas till lägre än NCAV har i regel nån form av problem och kan i vissa fall rentav vara konkursmässiga, vilket reflekteras i de mycket dystra framtidsutsikter som marknaden ger ett företag med denna värdering. Grahams idé är att man genom att systematiskt köpa bolag för mindre än de är värda, och att NCAV är ett konservativt sätt att bedöma hur mycket ett bolag är värt, över tid kan hålla en hög avkastning. Graham själv har uppgett att han med höll över 20% i årlig avkastning under lång tid genom att investera i net nets. Under sin tidiga investeringskarriär ägnade sig även Warren Buffett åt investeringar i net nets med mycket gott resultat, enligt egen utsago över 50% om året, efter att ha formats av Graham i sin investeringsfilosofi. Även Walter Schloss, en annan lärljunge till Graham erhöll goda resultat genom att applicera denna strategi under lång tid.

Akademisk litteratur

I en studie av Oppenheimer från 1986 undersöker författaren hur Grahams NCAV-strategi skulle ha presterat i USA över perioden 1970-1983. NYSE, AMEX och OTC-börserna inkluderades samtliga i analysen. Aktierna köptes sista arbetsdagen i december varje år, och enbart aktier som handlades till 66% av NCAV ingick i portföljen, i linje med Grahams föreslagna strategi. Innehaven hölls sedan i 12 eller 30 månader. Innehaven viktades jämnt.

Strategin där man håller bolagen i 12 månader resulterade i en genomsnittlig månadsavkastning på 2,45% att jämföra med 0,96% för NYSE-AMEX index under perioden, och 1,75% för ”Small-Firm Index”. 10 000$ investerade i net net-strategin sista december 1970 hade i teorin förvandlats till 254 973$ den sista december 1983, en CAGR om 28,2%. Motsvarande summor för NYSE-AMEX och Small-Firm Index var 37 296$ och 101 992$. När man justerar för risk, vilket i vanlig ordning definieras som volatilitet i den akademiska litteraturen, minskar överavkastningen till 1,46% per månad jämfört med NYSE-AMEX och 0,67% per månad jämfört med Small-Firm Index. Detta indikerar att net net-strategin är mer volatil än ett brett marknadsindex. Strategin där bolagen hålls i 30 månader visar likartade resultat med tydlig överavkastning.

Studien visar även att det finns ett förhållande mellan hur liten andel av NCAV man betalar och framtida avkastning. Ju lägre P/NCAV, desto högre avkastning.

En studie från 2010 av Carlisle (samma Carlisle som idag har podcasten/fonden The Acquirers Multiple), Mohanty & Oxman tar vid där Oppenheimers studie slutade, och undersöker samma strategi med 12 månaders innehav för åren 1984-2008. Resultaten från denna studie är i linje med Oppenheim, då net net-strategin ger en genomsnittlig månadsavkastning på 2,55% att jämföra med 0,85% för NYSE-AMEX och 1,24% Small-Firm Index. Detta indikerar att net net-strategin överavkastar NYSE-AMEX index med 22,42% och Small-Firm Index med 16,9% årligen.

Även i denna studie testar författarna även att hålla innehaven i 30 månader, vilket ger en månatlig överavkastning om 2,56% för net net-portföljen, men med stor variation längs vägen.

När man delar in innehaven i portföljen i kvintiler baserat på hur stor andel av NCAV man betalade för aktien så får man i denna studie, till skillnad från Oppenheimer, resultatet att de billigaste innehaven faktiskt presterat sämst. Den andra kvintilen, d.v.s. de näst billigaste innehaven som grupp har däremot presterat bäst, därefter är ordningen linjär. Studien försöker även förklara överavkastningen med hjälp av andra konstaterade effekter såsom värdepremien, storlek på bolagen, momentum, likviditet m.m. Man konstaterar att överavkastningen inte kan förklaras bort genom att bolagen är ovanligt små, värdeeffekten, eller genom högre marknadsrisk. Likviditetspremien, att bolagen som ingår i strategin generellt har lägre likviditet än index, förklarar en viss del av överavkastningen, men långt ifrån hela. Författarna konstaterar även att strategin inte tycks ha presterat sämre med tiden för den period som undersökningen omfattar.

Redan 1981 genomförde den mycket kända investeraren och författaren Joel Greenblatt en studie på ämnet tillsammans med Richard Pzena och Bruce Newberg. Metodiken här var annorlunda. Man filtrerade till att börja med bort bolag med ett marknadsvärde under tre miljoner dollar, och tittade sedan enbart på aktier som börjar på bokstäverna A eller B för åren 1972-1978. Från dessa 750 kandidater som kvarstod bildade man fyra olika portföljer, där innehaven antingen handlades under NCAV, handlades under NCAV OCH hade ett PE mindre än 5, handlades under 85% av NCAV eller slutligen handlades under 85% av NCAV OCH hade ett PE under 5. Innehaven såldes efter en uppgång på 100%, eller efter två års tid. Innehaven var även här jämnt viktade.

Samtliga portföljer överavkastade index med råge, med årliga avkastningar mellan 20-42,2% före avgifter och skatt. Den portfölj som nådde hela 42,2% avkastning var den portfölj där bolag som både hade ett P/NCAV under 0,85 och ett PE under 5 ingick i portföljen. Det går dock att rikta viss kritik mot denna studie. Dels täcker den ett ganska kort tidsintervall, och dels är vissa av kraven för att inkludera bolag i en portfölj så strikta att antalet bolag i portföljen blir väldigt få, under vissa år var vissa portföljer inte ens investerade alls i marknaden. Detta är å andra sidan kanske mindre förvånande när man betänker att författarna enbart tittade på bolag vars namn började med A eller B och därmed hade ett klart mindre urval av aktier att välja från än vad som är fallet i praktiken.

En studie av Xiao & Arnold testar en net net-strategi på London Stock Exchange för åren 1981-2005. Här är kriteriet för att ingå i portföljen att NCAV / Marknadsvärdet för bolaget ska vara minst 1,5 vilket alternativt uttryckt ger ett P/NCAV < 0,5. Även i denna studie överavkastar strategin på ett sätt som inte kan förklaras genom kontrollerande variabler. Man provar i studien innehavsperioder om 1-5 år och testar både jämviktade portföljer samt marknadsviktade portföljer där ett innehavs vikt i portföljen står i relation till bolagets marknadsvärde. Den jämnviktade portföljen presterar bäst med årlig avkastning på över 31% i det fall då innehaven ombalanseras efter 12 månader, och 254% avkastning över fem år i det fall då innehaven hölls i just fem år, vilket motsvarar en CAGR om 20%.

An, Cheh, Kim fastslår i en studie som omfattar USA för åren 1999-2012 att net net-strategin tydligt överavkastar S&P 500, men med högre standardavvikelse. Avkastningen ligger runt 17-18% per år för de olika portföljerna. Denna studie visar även att strategin faktiskt går sämre än indexet i perioder då marknaden har negativ avkastning, men att detta kompenseras med råge av att strategin avkastar klart mer än indexet i perioder då marknaden går uppåt. Man föreslår därför en hedge-strategi för att begränsa volatiliteten, vilket ökar den totala avkastningen till 24-30% årligen för de olika portföljerna.

Det finns även en studie som jag inte har full tillgång till som visar att strategin överavkastar även på den japanska marknaden. Hur stor överavkastningen är och för vilka år detta gäller framgår ej av sammanfattningen i länken ovan.

Net nets har även undersökts i flertalet böcker. Enligt Victor Wendls bok ”The Net Current Asset Value Approach to Stock Investing” gav net nets en avkastning på 27,7% per för åren 1950-2009, de år portföljen var fullinvesterad. Här filtrerades så att bolagen behövde ha ett marknadsvärde på minst 30 miljoner dollar. James Montier skrev i boken ”Value Investing” att han uppnått en avkastning på 35% per mellan 1985-2007 för en global net net-strategi, och ovan nämnda Tobias Carlisle rapporterade i sin book ”Deep Value” att net nets gav en avkastning om 38,7% om året 1970-2013. Sammantaget är det empiriska stödet för att net nets i teorin ger en mycket god avkastning, framför allt på den amerikanska marknaden fram till 2012, mycket starkt.

En masteruppsats från Linnéuniversitet av Karlsson & Strand undersökte flera mekaniska investeringsstrategier på den svenska marknaden för åren 1998-2016, bland dessa net nets. Denna studie visar att net nets har underpresterat index i Sverige under denna period. Detta är dock i min mening en sanning med modifikation. När portföljerna byggdes varje år skulle dessa bestå av 10 innehav, lika viktade. I det fall då det inte fanns 10 net nets att fylla portföljen med i starten av ett år fylldes portföljen istället ut med den riskfria räntan. Om man exempelvis hade fyra net nets att tillgå bestod portföljen till 60% av den riskfria räntan. För år 2011 fanns ingen net net, varför hela portföljen bestod av riskfria räntan. För åren 1998, 2006, 2007, 2014, 2015 bestod portföljen av ett bolag och 90% riskfria räntan. Endast två år, 2003 och 2009, bestod portföljen av 10 net nets. Att på denna grund påstå att net nets underavkastar index är därmed inte korrekt, men det visar likväl på det faktum att det sannolikt är omöjligt att använda sig av en mekanisk net net-strategi om man begränsar sig till svenska bolag, då det helt enkelt inte finns tillräckligt många att tillgå.

Kritik

Att net nets som strategi fungerat historiskt är tydligt. Stödet är starkast i USA där flertalet olika perioder undersökts, men samtliga studier jag stött på som tittar på internationella marknader bekräftar att strategin tycks överavkasta även på dessa. På senare år tycks det dock som att net net-strategier, precis som övriga mekaniska värdestrategier, haft svårt att hålla jämna steg med marknaden, åtminstone på den amerikanska marknaden. Vad beror detta på, och hur sannolikt är det att denna trend kommer att bestå?

Som Evan Bleker skriver på sin sida netnethunter.com har detta delvis att göra med att en betydande andel av net nets på 2010-talet i USA har varit kinesiska bedrägier, och om man exkluderar dessa ser resultatet bättre ut för strategin. Med det sagt finns det även rimliga argument för varför det skulle vara svårare att genomföra strategin på ett lyckosamt sätt idag, då all information är mycket mer lättillgänglig för gemene man idag, vilket kan leda till att detta arbitrage inte längre är möjligt då det kan snappas upp snabbare av både robotar och en större pool manuella investerare som letar efter just dessa typer av bolag. Å andra sidan är det knappast net nets som fyller mitt Twitter-flöde om dagarna, och den typ av bolag som net net-portföljer i regel består av (små, illikvida bolag med tråkiga verksamheter och svaga resultat) är alltjämt den typ av bolag som många investerare skyr som pesten just på grund av dessa egenskaper. Strategin har också tenderat att fungera som allra bäst då marknaden varit på väg upp efter en svag period. Då vi bortsett från det dramatiska Corona-raset inte haft en längre nedgång på börsen på många år, är det inte alls omöjligt att strategin kommer att göra en stark comeback efter nästa stora svaga börsperiod. Detta talar i min mening för att strategin bör kunna fungera även framgent. Det finns även vissa anekdotiska bevis i form av Henning Hammar som under perioden 2016-06-30 – 2018-04-03 nådde en avkastning på 72% i sin net net-portfölj, och tidigare nämnda Evan Bleker som enligt egen utsago haft en CAGR på 22% i portföljen 2014-2019 enbart genom att investera i net nets (dock ej helt mekaniskt) som antyder att strategin alltjämt fungerar utanför USA.

Det finns även viss kritik kring metoden i studierna. Aswath Damodaran menar i en blogpost från 2010 att överavkastningen som flertalet mekaniska strategier uppnår i teorin via backtest inte skulle gå att replikera i verkligheten på grund av transaktionskostnader. Dels pekar han på courtagekostnaden som kommer att dra ned avkastningen (detta kontrolleras det dock för i flera av studier nämnda ovan), men en mer intressant poäng som är väldigt relevant i fallet med net nets handlar om spreaden mellan ”bid” och ”ask”. De flesta bolag i en net net -portfölj är små och illikvida. Ska man handla dessa är det inte alls omöjligt att man med sitt köp forcerar upp kursen något för att fylla sin position, och att man när det är dags att sälja trycker ner kursen något för att bli av med sitt innehav. Detta leder till en sämre avkastning än dessa teoretiska studier där man inte behöver köpa eller sälja innehaven i praktiken, utan bara använder de citerade kurserna för respektive köp/säljdag i analysen, indikerar. Denna kritik är i mitt tycke helt befogad och jag finner det sannolikt att praktiskt avkastning för dessa mekaniska strategier är något sämre i verkligheten. Det är dock svårt att veta exakt omfattning av denna effekt, och eftersom alla studier pekar på en årlig avkastning om minst 20%, ofta upp emot 30%, finns det gott om utrymme för dessa kostnader att påverka avkastningen utan att denna ska gå ner hela vägen till en marknadsmässig avkastning om 8-10%.

Ett mer praktiskt bekymmer för den gemene investeraren tror jag är volatiliteten. Det är genomgående i alla studier så att standardavvikelsen i net net-portföljerna är högre än för marknaden som helhet. Volatilitet är alltid svårt att hantera, och klarar man inte av att hantera de svängningar som strategin innebär finns en stor risk att man inte genomför strategin på ett bra sätt, utan ger upp längs vägen. Strategin kommer inte att överavkasta varje år, det kan (som det nu gjort i USA) gå flera år på raken där strategin inte levererar. Det är svårt att hålla fast vid en strategi som underpresterat i flera år, och detta problem är enligt mig den största svårigheten med att genomföra en net net-strategi i praktiken.

Sammanfattning

Resultaten från dessa studier tål sannerligen att tänkas på. Går det att uppnå 15-20% eller till och med 25% årlig avkastning med en mer eller mindre mekanisk strategi är detta ett mycket lockande alternativ, då väldigt få investerare lyckas hållas denna avkastning över tid. En nedsida är dock volatiliteten, som kommer att vara större än om man följer ett index. Nedgångar på 50% av portföljen kommer vara vanligare, och detta är något som är otroligt svårt att hantera normalt sett (vilket vissa av oss blev varse för bara några månader sedan), och kanske är det ännu svårare om han har en portfölj bestående av enbart mediokra bolag till ett riktigt bra pris. Det är lätt att tappa sin tro till även de starkaste bolag i de tuffaste mentala perioderna, och överger man sin strategi när det blåser som värst riskerar man sannolikt att gå miste om de allra mest lukrativa perioder som med denna strategi tycks följa de allra tyngsta perioderna. Ska man investera i net nets måste ha en stor tilltro till strategin, så att man även i de tyngsta perioder härdar ut och låter volatiliteten ha sin gång för att sedan skörda frukterna. Man måste även vara villig att investera utanför Sverige, då antalet net nets som dyker upp här är för få för att basera en investeringsstrategi på. För att hitta kvalitativa net nets, vilket möjligen kan få en att må lite bättre över sin portfölj i tuffare tider, behöver man sannolikt lägga ner en hel del jobb även på denna strategi för att hitta potentiella bolag i många olika länder världen över. Historisk avkastning är som alla vet ingen garant för framtida avkastning, men om det är så att strategin kommer att generera framtida avkastning ens i närheten av teoretiskt historisk, är det ändå svårt att föreställa sig ett enklare sätt att erhålla en riktigt bra avkastning.

Om du är intresserad av diskutera net nets eller har tillgång till fler studier som jag borde läsa och vill dela med dig av dessa, maila mig gärna på perplexedinvesting@gmail.com

This is just a very short post aimed at my miniscule group of readers that are from outside of Sweden. From now on, I will be writing in Swedish, as the vast majority of readers are from Sweden anyway. Going forward, I will try to write a little more often, and as such I will mix some more theoretical posts with regular reports on companies that I have researched in the past. My goal is to post once a week.

Disclaimer: The information provided in this post is not to be considered as any form of investment advice. I might buy or sell shares in any companies discussed in the post without notifying readers of the blog. I currently own shares in TGS-Nopec Geophysical Company.

I don´t think anyone even remotely interested in finance have missed what has happened with the oil price as a consequence of the drastic drop in demand due to the spread of the Corona virus, and the subsequent price war between Russia and Saudi Arabia. I will not go into details on that at all as I am no expert on oil by any means, and there is plenty of reading material out there on the subject if one wishes to get additional information on that subject.

However, I do like to be a little contrarian and look at things that people are avoiding at the moment, for one reason or another. As such, oil companies make for interesting hunting grounds having lost a significant portion of their market values in a short period of time. I would guess that the very best returns in the oil sector can be made if you identify levered companies that are valued as if they are going bankrupt but make it through, but since I have a preference for qualitative companies with strong balance sheet, that is not the route I have taken. Instead I will provide a brief overview of two companies with asset light business models and strong balance sheets that I think are attractively valued right now. This will not be in depth at all, and again, I am no export on oil so please do your own dilligence before buying anything I might have written about on the blog. I have no idea what the oil price will be in one month, six months, a year or even several years out, but I do think that the current oil price is unsustainably low, that the world will require oil for a long time to come, and that these two companies will be valued much higher when the oil price eventually regresses to a more normal level, with a very low probability of going bust in the interim.

TGS-Nopec Geophysical Company

This is a company listed on the Norwegian Oslo Exchange that I have owned for a long time, but that I have added to during the rapid fall in stock price from a high of over 280 NOK in mid December to around 138 NOK as I write this (it was tradig below 100 NOK at one point i March). TGS does not produce any oil, instead it collects, processes and provides seismic data to E&G companies. They are one of the leading global companies in the sphere with a multi-client business model where they collect the data once, and then sell the same data to several different clients. Generally, a decent portion of their revenues are pre-funded, meaning that the customer funds the exploration beforehand, reducing capital needs. The company does not own any vessels or crews for data gathering, instead they rent or do joint ventures with other companies that provides the vessels and crews. As a consequence, the fixed cost base is quite low and the company can be quite agile in crisis times like these and cut investment in the multi-client library quickly and remain cash flow positive.

Investments are continually made into growing the data library. Since the inception of new accounting rules in 2016, the library is being amortized aggressively, currently at a higher pace than new investments. As a consequence of this, the fact that a portion of the explorations are pre-funded by customers and the overall asset light, low fixed cost business model, the company generates a lot of cash flow compared to earnings. Free cash flow is typically higher than EPS. The company is free of debt and had net cash of abount 3 billion NOK at the end of Q4 2019. Free cash flow after investments in the multi-client library has been positive every year for as long as I have looked at the data in depth (2010).

During 2019, the company acquired Spectrum, another Norwegian company with a very similar business model but with a complementary data library, so to make reasonable predictions about the future, you need to look at the history of both companies and make some reasonable assumptions about future growth and potential synergies. Furthermore, the business is quite cyclical as customers investment behaviour with regards to new explorations are heavily influenced by the current oil price, so you need to use several years of data to estimate future earnings power, to get a sense of what the business will do over a full cycle. TGS has already warned that 2020 will be a challenging year, but thanks to their business model I still expect them to remain cash flow positive. Historically TGS has had a counter-cyclical investment policy where they invest more relative to peers in rough times for the industry to gain market share in the long-run. They have already announced a cut in investments in the multi-client library for FY2020 from 450 MUSD to 325 MUSD, which is still higher than the 250 MUSD that peers planned to spend on average before the Corona virus outbreak.

The company pays a quarterly dividend. They were planning to pay 0.375$ per share and quarter, but in light of recent events they decided to cut the next quarterly dividend to 0.125$ per share, and will evaluate the situation further going forward before deciding on what will happen to the divident for the rest of the year. They have historically also bought back stock continually, hopefully they felt confident enough to do so aggressively when the stock price plummeted in March. If not, I would have rather seen a complete suspension of the dividend in favor of buying back shares.

If we look briefly at valuation, EV should be around 13 billion NOK. Free cash flow defined as operating cash flow minus investments in the library for 2019 was about 2.1 billion NOK, and EBIT around 2.3 billion. These numbers only include Spectrum from the date the acquisition was closed in late August so on a full year basis were a bit higher for the combined entity. This gives multiples of EV/FCF2019 of a little over 6, and EV/EBIT2019 just under 6. Now, 2020 clearly wont resemble 2019, and judging a cyclical business on the results of a single year is probably not the best idea. Combining historical data for TGS and Spectrum with some assumptions on synergies based on what has been communicated, I end up with normalised FCF of around 1.6 billion NOK. This would give a EV/FCF of 13/1.6 = 8.125 or a a FCF-yield of over 12%. This might be a little aggressive given that 2020 will proably be quite weak, but given that I also expect the company to grow at maybe 3-4% a year over a full cycle I still think that a return of well over 10% seems very doable. If the stock price gets back to the December high (it has traded even higher previously) of 280 NOK in lets say five years, that would give a compounded annual return of almost 15% excluding any dividens or buybacks. This is certainly not the most explosive upside you can find in the industry, but it is a very safe company with a proven business model that generates a ton of cash. There are certainly risks here as in all businesses, but at least the risk of the stock going to 0 should be incredibly low.

Tethys Oil

I first started looking at Tethys in the fall, when it traded around levels of 80 SEK, and found it really cheap. Thankfully, for various reasons I didn´t pull the trigger, and now the stock has dropped to a price of around 47-48 SEK per share.

Tethys Oil is listed on the Stockholm Exchange in Sweden, is head quartered in Sweden and has a Swedish CEO. However, pretty much all of their revenue is generated in the sultanate of Oman. In fact, it is generated from one single source in Oman, namely their license to get a 30% production cut of the production in Blocks 3 & 4 in Oman. They are not the operator of the license, so they have very little tangible assets on the books. They do own a license in Block 49 in Oman where they are the operator and are currently about to start drilling for oil, but so far no commercial production has been commenced. The company also holds a share of the license in Block 56 where they are not the operator, and as in the case of Block 49, this has not generated any revenue to date.

Oman has historically been politically stable and has managed to stay out of any major wars despite their sensitive location. However, a quick search on Google makes it evident that human rights isn´t exactly on top of the agenda, and that the finances of the country are quite poor. To complicate things further, the government takes a share of all the production of oil in the country. In Tethys case, the license holders first get reimbursed for the costs of running the well. This is called cost oil. Any profits above costs are then shared beetween the government and the license holders. As far as I can tell, the budgets are made annually so Tethys share of output varies from year to year and could in theory vary all the way from 20% to 52% of the 30% of production that belongs to Tethys within their license. Historically though, Tethys share has been around 50-52% for most years, and they have guided towards a production share of 52% for FY2020. To date, Tethys seems to have had no problems at all operating in Oman and given that they are attaining more and more licenses in the country, they seem to have a good relationship with the state. That said, generating almost all revenue from a single license in a country located in a part of the world that has been very politically unstable for quite some time, with a leader that has absolute power of just about everything that goes on in the country, seems like something that deserves quite the risk premium.

So on to the numbers. For the last four years, Tethys share of production has been quite stable at around 2.2-2.3 million barrels of oil, so any differences that you might see in revenue is mostly due to volatility in the oil price. In 2019, with an average oil price of 64.2$, Tethys EBIT was 37.1 million USD which translates to about 374 million SEK. Average EBIT for the last three years is 45 million usd, for the last five years it´s around 32 million USD. In 2016, with an average oil price of 40.5$ they had negative EBIT of 0.4 million USD.

As I write this the stock price of about 48 gives a market cap of around 1.6 billion SEK. Tethys has no debt, and net cash of around 760 million SEK rendering an EV somewhere around 840 million SEK. EV/2019 EBIT is something silly like 2.4, EV/2019 FCF just over 3. So yeah, that’s incredibly cheap. If we use the five year average EBIT of roughly 320 million SEK we still get an EV/EBIT of less than 3.

As I mentioned, the company lost money in 2016 when the average oil price obtained was just over 40$. Cash flow was slightly positive. The company recently announced that they are taking measures to make sure they remain cash flow positive even at oil prices of 30$, so the risk of the company going bankrupt and the stock going to 0 should be incredibly small in this case as well. Clearly though, as is the case with TGS, in order for this bet to work out, oil prices need to revert to more normal historical levels eventually.

Tethys has historically returned a lot of capital to shareholders. In 2019 they paid an ordinairy dividend of 2 SEK and returned an additional 6 SEK per share through a mandatory redemption program. The plan was to do the same in 2020, but in light of recent events they have lowered the additional return to 3 SEK, while keeping the ordinariy dividend of 2 SEK, so 5 SEK in total will be returned to shareholders putting the ”dividend” yield above 10%.

As long as you believe that oil prices will eventually revery, then Tethys looks incredibly cheap, no matter how you slice or dice it. Still, I don´t own the stock. Why? Well, so far, I have had a hard time coming to terms with the geographical and political risk. Even though there have been no problems operating in Oman so far, and the country hasn’t been involved in any major conflicts yet, there is no guarantee that the same will hold true going forward. Also, any kind of force majeure event that could strike the region and wipe out production in the area would completely wipe out Tethys revenue along with it. Also, there is simply no way around the fact that the faith of Tethys is completely in the hands of the government of Oman, or more precisely, the sultan/chief of staff of armed forces/minister of defence/minister of foreign affairs/chairman of the central bank (yeah, it´s the same guy). Additionally, I don´t want to allocate to large of a portion of my portfolio into oil, and since I like TGS way better as a long term holding, that has been my choice in the sector so far.

That said, I am still interested in Tethys. First, I need to decide whether the risks described above makes the company uninvestable for me. If not, I need to figure out what price would make it worthwile to assume all these risks, which of course, is a function of the potential upside as well. A company with a single revenue generating asset like Tethys will probably never get any sort of premium valuation, as was evident in the share price even before this whole oil mess started. That said, even a defensive multiple of say 6 times normalised EBIT would generate a very nice return, as long as that normalised EBIT actually happens. For the sake of argument, if we assume that 2019 EBIT is a good approximation for a normalised EBIT, a 6 times EBIT multiple on that would indicate an upside of like 150% on todays stock price. Even if that takes five years to achieve, you´re looking at a 20% annual CAGR excluding any dividends.

As always, I greatly appreciate any feedback. This was not meant to be a deep dive in either company, but rather a brief pitch to provide you with two potential ideas to do further work on. Thank you for reading!

Disclaimer: The information provided in this post is not to be considered as any form of investment advice. I might buy or sell shares in any companies discussed in the post without notifying readers of the blog. I currently do not own shares in Points International.

It´s been quite some time since I last wrote something on this blog, about two and a half months in seems like. A lot has happened since, to say the least, and it actually feels like it´s been a lot longer.

First of all, I should probably mention that I have sold all my shares in Points International. It is hard to imagine a worse scenario playing out than what is happening right now for a company with massive exposure to the travel and hospitality sectors. When the company released it´s Q4 Earnings Report on March 4th, they reported that they had not yet seen a material impact from the COVID-19 virus outbreak, and that airlines historically in times of low passenger traffic had used other sources of revenue such as their loyalty programs to a larger extent to compensate for lost revenue. However, people just aren´t flying or even travelling right now unless it is absolutely necessary, and might not do so for quite some time, and over time I imagine that this has to hurt the business. This is obviously a temporary thing and not detrimental to the business long-term as they carry no debt, but I do fear that revenue will plunge to such an extent that they might end up having to buy loyalty points from their partners due to not reaching the annual guaranteed revenues that they give to their customers, which could change their balance sheet drastically if they were to assume debt and carry loyalty points on the balance sheet. Also, there is a real chance that airlines could go bankrupt and that Points lose business that way. I could very well be proven wrong, in which case I will tip my hat in respect to the company. If they actually manage to get through this without a severe drop in revenues, the company is way more resilient than I thought and I would be more interested than ever in owning the company. I do continue to the follow Points with great interest, and might certainly own it again the future, depending on the outcome of this crazy situation.

I don´t regret buying Points, and I do not regret selling it either. Sometimes, a low probability event that smash your thesis to bits occurs, in which case you just have to accept it and move on. That does not have to mean that your initial analysis was wrong or that you made a bet with a negative expected value. I could have probably been a little bit quicker in reacting, but overall I don´t have any major problems with how I handled the situation with Points.

I try to reflect on how I´ve handled this very tumultuous time in the market overall, and learn from it. Given that I´ve played poker for a living for many years, I´m probably more used to daily swings and losing money than most people, but I have to admit that it still hurts to see you portfolio drop 30+% in a very short period of time, even though I am well aware that in a lifetime of investing, this is likely to happen many times, and that we might still be far from reaching a bottom. It is very easy to let your emotions get the best of you and make irrational decisions, that are likely to mimic the emotional behaviour of the rest of the market, i.e. selling what everyone else is selling at the same time, and buying what everyone else is buying at the same time, or not buying at all. I don´t think that I have panicked during this crisis, but I might have made a decision or two that was a bit rushed, buying into something where I wasn´t really done analysing it because the price dropped by a lot in a short period of time, without really knowing what I estimated it´s intrinsic value to be. Hopefully I will learn from this and not repeat that same mistake in the future. Having patience and the ability to keep calm and rational is incredibly important, and something else I have learned about myself during this very volatile period in the market is that conviction in your holdings is crucial. If I feel confident that the value of the company is greater than the current price and that the business will be fine long-term, it just makes it so much easier to ignore the current share price as well as other random noise, and focus on what is important.

My overall strategy remains the same. I do not believe in timing the market, as there is ample empirical evidence that shows that this is a fools errand. Since I don´t plan to use the money that I have invested in the stock market for a long time, and I feel very good about the chances of all my holdings compounding at a rate of well above 10% for the years to come, I remain more or less fully invested. As I write this I happen to have some cash lying around from selling Points, but it will put to use as soon as I find a case that I feel confident about. But learning from previous mistakes made, I try not to rush it. I´m sure there will be many great opportunities going forward and as I mentioned above, I really want real conviction when buying into a new business.

I see a lot of people discussing macro stuff and selling of or hedging in my social media feeds. Some of it probably has to do with people using very different strategies from mine, but as far as I can tell, a lot of it is also driven by fear and the notion that one can know perfectly well when to enter or exit the market. The number of tweets I have read with people saying that they are ”waiting until things have settled down to get back in” are probably in the hundreds. The problem is that we will never know when things have settled down, or when the market has bottomed. If nothing else, the volatility from the last month goes to show how incredibly fast markets moves these days, and once things start to look better across the world, the market might be very quick to react. Or they might not. Thats the point. We just dont know. And honestly, who really knows the implications this whole thing will have on the economies across the globe? I sure don´t. I have no opinion as to whether we´ve bottomed out now, or whether it will take five years to do so. What I do feel confident about, is that if I left my portfolio untouched for ten years, it will be worth a lot more by that time, or at least some time during this 10-year period. With my time horizon, I would also guess that now is likely a better time to buy stocks than six months ago, as (some) valuations have come down quite a bit. Since I try to stay fully invested at all times (provided I have enough ideas) that part isn´t as important to me, but it is something to keep in mind if owning stocks right now feels awkward. Even with a 3-7 year holding period, the price you pay affects your return quite a bit, and even if future prospects have become significantly worse (and hard to perfectly determine) for some companies, there are also companies out there that have become a lot cheaper without this whole episde changing their outlook much, or in some cases not at all.

Investing in volatile times is emotionally hard, but I honestly feel that it is in times like these that you can actually add a lot of value by not being caught up in the market panic, and to instead stay calm and rational. I also think that since these instances are (thankfully) rare, you have to take the opportunity to really try and learn from them, and this is the key, without being short-sighted or results oriented. I have certainly learned a ton about how markets function in times of crisis, and maybe even more so, how I function in times of crisis. I hope that will pay off for many years to come.

Disclaimer: The information provided in this post is not to be considered as any form of investment advice. I might buy or sell shares in any companies discussed in the post without notifying readers of the blog. I currently own shares in Points International.

My latest position is in Points International, a Canadian company providing e-commerce and technology solutions to the loyalty industry headquartered in Toronto, trading both on the Toronto Stock Exchange (ticker PTS) and on the NASDAQ stock exchange in the US (ticker PCOM). Over 90% of the daily trading volume happens in the US. Market cap is around 200MUSD and the annual share turnover is roughly 80%. It is a small/micro-cap company that is fairly illiquid, and thus might have potential to be overlooked by the overall market.

BUSINESS

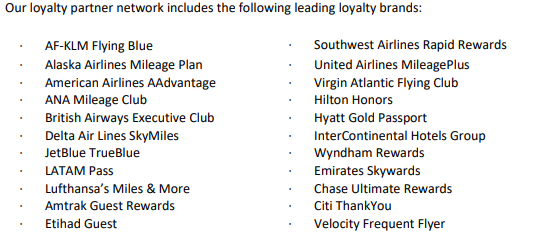

It is not entirely straightforward to figure out exactly what it is Points does exactly. Citing the companies filings, they are the “..global leader in providing loyalty e-commerce and technology solutions to the loyalty industry, connecting loyalty programs, 3rd party brands and end consumers across a global transaction platform.” Points do not run their own loyalty programs, and they do not provide the technology to operate such a program. Instead, they have build a “Loyalty Commerce Platform” (LCP) that loyalty programs and third parties can use for transaction capabilities, program integration, analytics, reporting, security and fraud detection. The products and services offered by Points are designed to increase loyalty programs revenue and profits by selling loyalty program currency or related services to end consumers or third parties, drive efficient cost management by offering “non-core redemptions” and to enhance loyalty program member engagement. In short, Points partner up with loyalty programs and help them make more money through the use of their platform. Points have direct integrations with over 60 loyalty programs, with the majority belonging to the airline or hospitality space. The total number of loyalty program member accounts in the network of loyalty programs integrated with Points is over 1 billion. The loyalty industry as a whole is growing rapidly with the number of annual memberships up 15% a year (according to Points investors presentation). 60% of points/miles acquired in a year is estimated to be bought by 3rd parties such as Points. Below is a snippet from the annual report showing some of the major loyalty partners.

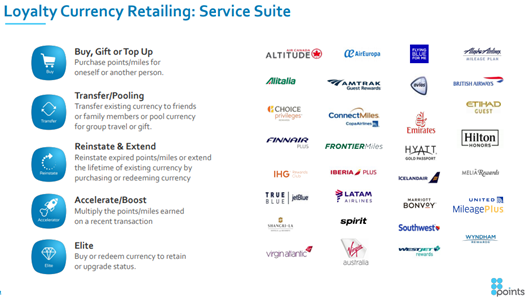

The company operates three different business segments. The, by far, biggest contributor of revenue (and pretty much entire contributor to profits) is the “Loyalty Currency Retailing” (LCR) segment. This segment consists of products and services to buy loyalty program currency for personal use or to give away as a gift, purchase status points to reach a tier status, transfer points to another member etc. In this segment, Points has 30 loyalty program partners that use at least one of the solutions within this segment, all within airline or hospitality. In this segment, Points primarily compete with the internal technology departments of the loyalty programs, but claims to have been successful in acquiring customers that previously provided the same services in house. Two thirds of the revenue within this segment comes from deals where Points technically acts as a “principal”, selling loyalty points at a retail price that they purchase at wholesale price from their partners. However, an important distinction needs to be made. Points do not load up on loyalty program points and keep them on the balance sheet. On the contrary, using the LCP, Points can buy the loyalty points in real time from their partner as they sell them to the end consumer. Importantly, Points get paid by the end consumer immediately and will have the money in their account within a few days, whereas the payments to loyalty partners are done on a monthly basis, usually 30 days after the end of the month in which a transaction was made. This leads to Points having “float”, usually with 1.5-2 months of revenue sitting on the balance sheet in cash at most times in payables to loyalty partners. Since Points seem to have very stable revenue streams from this segment, this float is essentially a free loan from the loyalty partners that pretty much funds Points operations and has enabled Points to grow without requiring any additional capital. Growth is essentially free for Points thanks to this.

The revenue where Points acts as a “principal” is booked on a gross basis. If someone buys 10 000 loyalty points through Points for 300$, but Points then passes 250$ along to the loyalty partner, the entire purchase amount of 300$ is booked as revenue, and 50$ becomes the gross profit on the transaction. For most other revenue within the business, what is booked as revenue is actually the commission that Points charges on transactions where they act as an agent or platform provider, on a net basis. Because of this, revenue isn´t a great measure to use when evaluating the company as a large chunk of that revenue is being passed along to loyalty partners and doesn´t belong to Points, though it is still crucial in generating the float that funds the operation. Gross profit is a better number as it is more indicative of the money earned by Points that will actually stay with the company permanently, it is essentially the “real” revenue for the business. Because of the way revenue is booked in this segment, the gross margin is quite low at around 12%.

In 2018, almost 98% of total revenue was generated in the LCR segment, and over 100% of operating profits. In the LCR segment, Points actually guarantees annual revenue to some of their major partners. For instance, in 2020, Points has guarantees to various partners to sell at least 150 MUSD worth of loyalty points in total. If they do not manage to do this, they will have to buy the loyalty points themselves from the partners, creating a potential liquidity risk. Revenue in this segment is likely to end up somewhere between 350-400 MUSD in 2019, so the total liability isn´t that great in comparison to total revenue. These liabilities are very likely to be spread out over several partners, so even though Points revenue in total is likely to stay way above the guaranteed 150 MUSD, they may still miss the guaranteed revenue targets for a particular partner and be forced to buy loyalty points from this particular partner by the end of the year. As far as I can tell from the annual reports, this has only happened once in the last ten years or so.

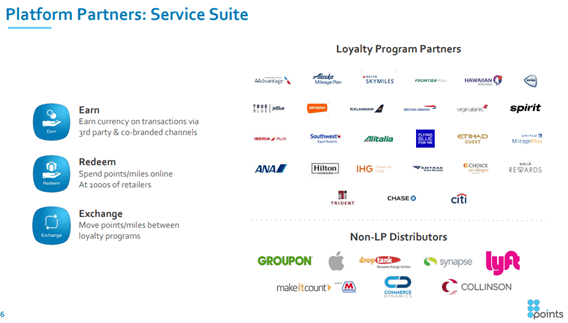

The other two segments are “Platform partners” and “Points Travel”. In the “Platform partners” segment, Points allows loyalty programs, merchants and other consumer service applications to use the LCP to distribute loyalty currency and loyalty commerce through multiple channels. Several third party applications are enabled by the LCP. They range from redemption based services that offer cost management solutions to loyalty partners, to earn-based services where merchants can partner with Points to buy loyalty currency to offer to their customers as awards. The revenue in this segment comes from commission fees, a set fee per transaction, revenue sharing or monthly recurring revenues, and gross margins are generally very high. In 2018 the segment generated revenues of just under 8 MUSD and a gross profit of 7.4 MUSD, with an operating result around 3.8 MUSD. I expect similar numbers in 2019.

The “Points Travel” segment is a white-label online travel service specifically designed for loyalty programs. Here, Points partner up with loyalty programs to enable members of the loyalty program to easily earn and redeem loyalty points by making hotel or car reservations online. By year end 2018, Points had 12 partners using at least one of their services in this segment generating a total of 1.8 MUSD in revenue (mostly from commissions) and an operating loss of 3.8 MUSD. The competition is fierce within this segment, as major online travel agencies are among the competitors. The development of this segment has been slower than anticipated by management, but according to a recent earnings call, the economics for the partners are great in this segment, as well as the unit economics for Points.

The contribution of “Platform partners” and “Points Travel” to the bottom line is very close to 0 for the time being, but even if they aren´t adding profits on their own, they might still be very useful. As mentioned, Points have a total of 60 loyalty partners, and offers a wide range of products and services within each segment. Whenever a new partner is signed, they usually just sign up for one or a few of the products that Points offers. Points then works on up-selling and cross-selling additional products and services to partners over time. If I´m reading correctly between the lines, both these segments, and maybe “Points Travel” in particular, is a great way to establish a relationship with a new partner that can be expanded over time. According the investor presentation, the current “opportunity matrix” within existing partners is only 30% penetrated, leaving ample space to grow with existing partners as well as new ones.

In December 2018, Points signed a strategic partnership with Amadeus IT, a giant IT provider for the global travel and tourism industry. Amadeus offers pretty much everything you can image, including loyalty programs, to airlines, airports, tour operators, insurers, ferry and cruise lines, travel agencies etc, and had revenues of almost 5 billion Euros in 2018. Citing the press release, the partnership “… will enable airlines to integrate Points’ solutions within existing Amadeus Loyalty Management and Awards solutions at the click of a button.” Amadeus have relationships with over 150 airlines across the globe, so if things turn out well, this could be a major driver of growth in the future, as Points look leverage Amadeus’ global presence and co-develop new services with them.

FINANCIALS

The financial results of the business has been pretty spectacular in the past. Revenue has gone up every single year since at least 2008 (this is the earliest year I have gathered data on), indicating that more and more loyalty points are being sold through the company every year. Adjusting for a one-time non-cash write down on a JV investment in China, gross profit has increased every year as well. EBITDA increased every year up until 2016 and 2017 when it decreased for two years straight, before increasing rapidly to record levels in 2018 with the company on track for another record year in 2019.

Looking back over the five year period of 2013-2018, gross profit has compounded at an annual growth rate of 10%, EBITDA at 14% and the companies favourite measure, Adjusted EBITDA at 16%. However, the company has bought back shares consistently since 2014, generating even greater growth rates per share with gross profit per share compounding at 21% annually for the period, EBITDA at 27% per share, and Adjusted EBITDA at 33%. If we look the period 2015-2018 instead, growth has been quite a bit slower with gross profit per share compounding at 11% annually, EBITDA 11% and Adjusted EBITDA 17%.

The business is generating a lot cash. In fact, it is one of the rare type of businesses that consistently generate more cash flow than earnings. Average after tax profit in 2013-2018 was 4.9MUSD. Average free cash flow (defined as operating free cash flow – all cash expenses for acquisitions of property & equipment and additions to intangible assets, as well as cash costs for the Restricted Share Unit-program) over the same period was 11.9MUSD. For the period 2015-2018, average after tax profit was 4.9 MUSD, and average FCF 11 MUSD. For the period 2013-2018, total after tax profits were 28.1 MUSD, total FCF was almost 60 MUSD.

The company achieved all of the above without carrying any interest bearing debt at all during any of the years I have data on, and they still don´t.

2019 is on track to become a record year in terms of both gross profit and adjusted EBITDA. Management has guided for gross profit to be between 58.5-64.5 MUSD which would mean 9-20% growth YoY, and adjusted EBITDA between 20.5-23.5 MUSD which would equal somewhere between 10-26% growth YoY. Additionally, during the year, the company announced long term goals of generating gross profits in the high-90 million dollar range by 2022, as well as more than doubling adjusted EBITDA to the mid 40-million dollar range. This is the first time that management has gone public with long term goals as far as I can tell.

MOAT

The financial performance of the company certainly seems to indicate some sort of moat. On a recent earnings call, one of the few analysts covering the call asked whether the company experienced any change in the competitive client regarding the LCR segment. Management reiterated that they did not, and that they mainly compete with the internal technology departments of their loyalty partners. For some reason, Points has managed to increase profits pretty much for 10 years straight, without seeing their returns competed away. Why is this?

If we consider the situation from an airlines point of view, they want to sell as many points as possible as rewarding and selling points has turned out to be a very lucrative business. Loyalty programs increases customer retention rates, which leads to a higher Lifetime Value (LTV) per customer. The more you can engage your customer, the higher the LTV over time. This has triggered loyalty programs to come up with new ways to generate revenue, for instance by offering members the opportunity to rent cars or make hotel reservations using their loyalty currency. So airlines wants to drive revenue in this segment, and they are faced with the choice of either building a product in-house and do all of the marketing themselves, or they could hire Points to do it for them. If they choose to build their own products to try and drive revenue, they are going to have to employ both capital and man hours to do so, with no guaranteed return on the investment. If they instead hire Points, they have no costs associated with this, and are instead guaranteed a steady stream of revenue as well as access to Points growing network of loyalty partners in other industries, primarily in hospitality.

Additionally, Points have access to transactional data and anonymized customer data from many different loyalty programs in the same industry. Without knowing for sure, I think it is reasonable to assume that this is an advantage when it comes to marketing as they should have more information to use to optimize any marketing efforts and generate a higher return on the investment than a single airline would on its own.

There´s also a scale component. An airline would have to spend X dollars to develop the products on their and market them. Points probably have to spend a similar amount, though I´m assuming the number is bigger for Points due to the fact that their customers might have different needs and requests, but they can then derive revenue from many different clients using the same technology, whereas the airlines would only derive revenue within their own loyalty program.

Lastly, there´s probably some network effects going on here. Points have established relationships with many partners in different sectors that an airline (or any other loyalty program) will get access to by partnering up with Points, meaning they don´t have to spend any time or money developing those relationships themselves. Developing new ways to earn or redeem loyalty currency is crucial to drive customer engagement, and getting access to Points network of merchants is a quick way of doing this. As an example of how this can work in practice, during the year Points signed a deal with Home Chef, one of the largest meal kit delivery companies in the U.S, that enables United Airlines loyalty program members to earn frequent flyer miles when they sign up for Home Chef. This way, Points benefits from any additional engagement from United’s loyalty members by selling more loyalty currency, as well as a commission from Home Chef whenever someone signs up using United miles.

Another example is the possibility for members of the Hilton Honors loyalty program to use their loyalty currency to pay for their Lyft rides, by leveraging Points LCP platform.

I am not sure quite how wide Points moat is. In theory, airlines and other loyalty programs might certainly in-house this type of products, but since Points generate more revenue and sign up more partners year after year, the trend seems to be the exact opposite. In theory, companies such as Amadeus with a massive network of partners in the airline industry and lots of resources that already run loyalty programs could easily build their own product to compete, but they didn´t. Instead they signed a partnership with Points. Other marketing businesses or transaction platforms could also be a potential threat, but the type of relationships Points has would probably take some time and resources to replicate, and it might not be worth it to an outside competitor as it is a very niche business. Really, it´s more like a part of the business of running a loyalty program, that Points has specialized in running on behalf of loyalty programs. Overall, it´s probably not the widest moat I´ve ever seen, but there are no signs at all that it is eroding at the moment.

MANAGEMENT & CAPITAL ALLOCATION

Management has generally been with the company for a long time. President Christopher Barnard and CEO Robert MacLean are both co-founders and have been in charge throughout the very successful history of the company, or at least as far back as I have gone in my research. While it is very nice to see continuity and a founder-led company by seemingly competent people, this makes the fact that insider ownership is quite low all the more puzzling. Barnard and MacLean owns just over 200 000 shares each, or approximately 1.5% each of the shares outstanding and are still the biggest shareholders of the board or management.

Since 2017, executives no longer gets cash bonuses. Instead, their entire bonus is paid out in stocks in a “Restricted Share Unit”-program. Rather than diluting shareholders, the company has decided to appoint a trustee to administer the program and purchase shares from the open market that are then passed on to management as bonuses. This creates a very real and recurring cash expense but keeps the number of outstanding shares lower, and should increase insider ownership over time. If you look at recent insider transactions, you see a lot of selling and not much buying. This probably is partly due to the fact that no one is given cash bonuses, so if you want any cash other than the base salary as an executive, you need to sell shares. With that said, if the company truly is reaching an inflection as management has said, it would be very comforting to see them load up on stock and put their money where their mouth is, or at least not sell any of the stock that is handed to them in bonuses.